.gif)

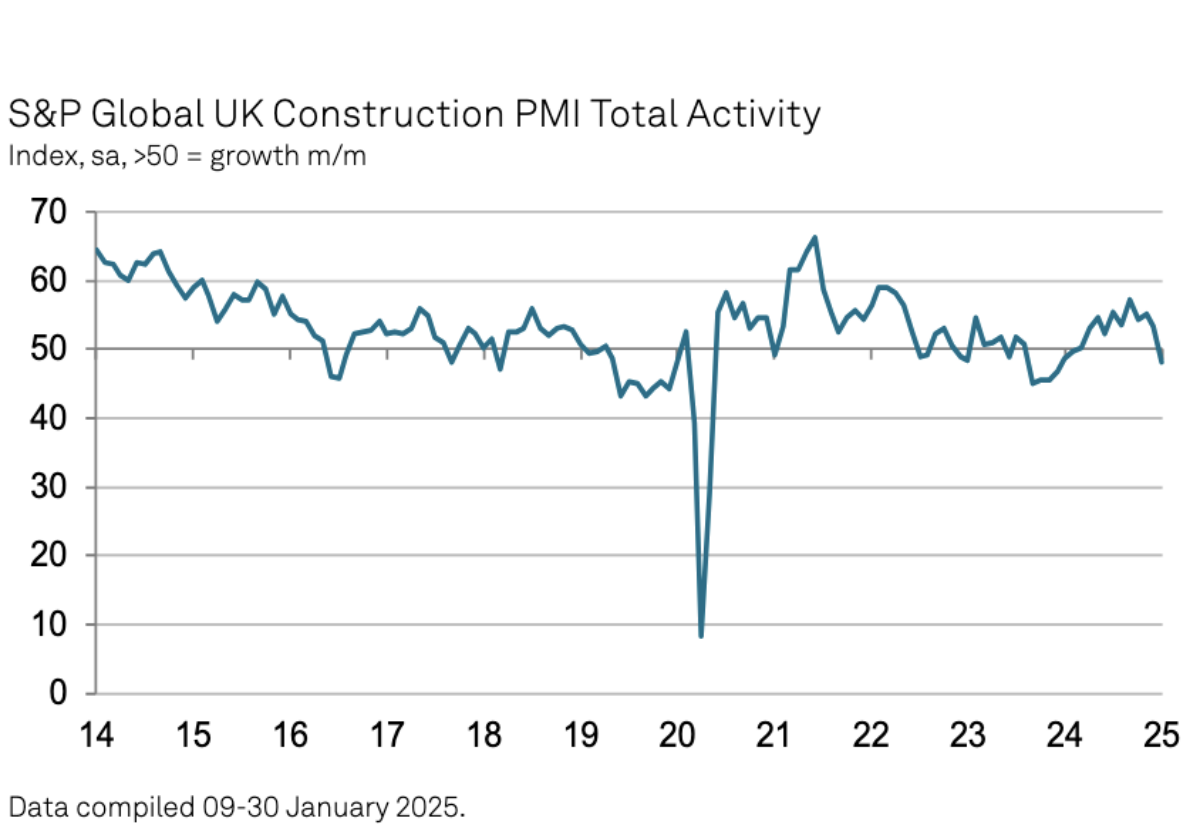

The bellwether S&P Global UK Construction Purchasing Managers’ Index (PMI) fell to 48.1 in January from 53.3 in December.

It was the first time the index registered below the 50.0 no-change threshold since February 2024.

Contractors blamed the fall on delayed decision-making by clients on major projects and general economic uncertainty weighing down business activity at the start of 2025.

Output fell across all sectors with residential hardest hit with the house building index at 44.9 which was a decrease for the fourth successive month and at the steepest drop since

January 2024.

Civil engineering activity (44.6) declined at a relatively sharprate, although this partly reflected disruptions from unusually wet weather at the start of the year.

Output in the commercial construction category also returned to contraction in January (48.9) linked to a lack of tender opportunities and a reluctance among clients to commit to new projects.

January data pointed to a decline in incoming new work for the first time in 12 months.

Although only modest, the rate of contraction was the steepest since November 2023.

Anecdotal evidence suggested that a lack of confidence among clients and worries about the UK economic outlook had contributed to fewer sales enquires.

Purchasing activity decreased for the second month in a row, reflecting weak order books and a lack of new work to replace completed projects.

Despite softer demand for construction products and materials, the latest survey indicated the steepest rise in input costs since April 2023.

Construction companies noted that suppliers had sought to pass on rising energy, transportation and staff costs.

Tim Moore, Economics Director at S&P Global Market Intelligence, said: “UK construction output fell for the first time in nearly a year as gloomy economic prospects, elevated borrowing costs and weak client confidence resulted in subdued workloads.

“Output levels decreased across the board in January, with particularly sharp reductions seen in the residential and civil engineering categories.

“Construction firms noted the fastest fall in residential work for 12 months as market conditions remained somewhat subdued. Anecdotal evidence suggested that caution regarding demand for new projects was prevalent at the start of 2025, despite strong policy support for house building and hopes for a longer-term boost to supply via planning reform.

“The forward-looking survey indicators were also relatively downbeat in January. New orders decreased at the fastest pace since November 2023 amid many reports of delayed decision-making by clients. Reduced workloads, combined with concerns about the general UK economic outlook, led to a dip in business activity expectations to the lowest for 15 months.

“There was little respite on the supply front, as transport delays meant that vendor lead times lengthened to the greatest extent for two years. Demand for construction items softened again in January, but purchase price inflation was the highest since April 2023 as suppliers sought to pass on rising energy, fuel and wage costs.”

.gif)

(300 x 250 px).jpg)